What is Blockchain?

A blockchain is like a digital logbook that permanently records transactions. It’s made of “blocks,” and each block contains a bundle of transactions—these could involve money, property records, agreements, or other types of digital exchanges.

Key Features of Blockchain

- No middleman needed (no bank or central agency)

- Transactions are verified by multiple computers in the network

- Once information is added, it cannot be erased or altered

- Works through the internet

Because of these features, blockchain is known for being secure and trustworthy. Let’s imagine how this works with a familiar example: a bank.

Traditional Banking Example

Suppose Alice wants to send money to Bob. In the traditional banking system:

- Alice’s money is stored in her bank account.

- The bank tracks her balance and lets her send money through online banking.

- When Alice sends a wire transfer to Bob, the bank updates both accounts.

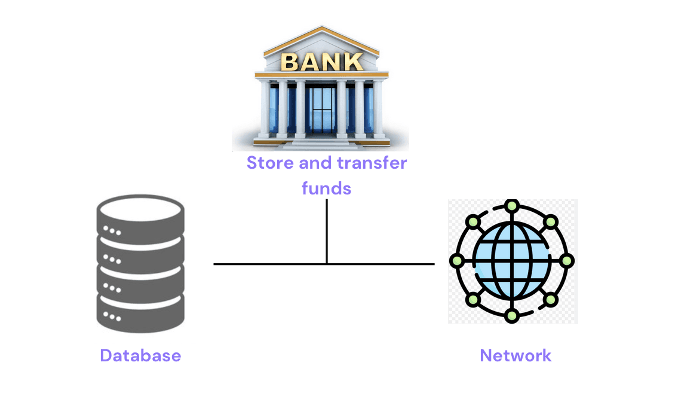

Behind the scenes, the bank uses:

- A database – to keep a record of all transactions and balances.

- A network – to process transfers between accounts.

How Blockchain Changes the Process

With blockchain, there’s no bank in the middle. Alice can send cryptocurrency directly to Bob.

Blockchain technology offers a different approach from the conventional banking model by removing the need for an intermediary such as a bank. Imagine that Alice wants to send money to Bob. In the banking world, she might use a wire transfer, relying on the bank to move her funds. With blockchain, however, she can send a digital currency (cryptocurrency) directly to Bob without passing through any financial institution.

Similar to how a bank provides a secure place to hold and transfer money, a blockchain allows Alice to store her digital funds safely and send them directly to Bob. In doing so, blockchain replaces two main technical roles that a bank typically performs:

- A system for recording balances – This tracks how much cryptocurrency Alice owns.

- A communication network – This connects Alice to other users (including Bob) so that transactions can take place.

A blockchain operates as a peer-to-peer (P2P) system, meaning it consists of multiple computers (called nodes) that communicate directly with one another. You can think of it as a globally distributed computer that performs the same roles a bank’s infrastructure would.

Every node in the blockchain network keeps its own identical copy of the transaction records. This redundancy makes the system extremely resistant to fraud or data manipulation. If Alice tried to alter her account balance dishonestly, the mismatch with all the other nodes’ records would immediately reveal the attempt.

Blockchain vs. Cryptocurrency

- Blockchain = the technology (like the internet)

- Cryptocurrency = one application of that technology (like email on the internet)

How a Blockchain Transaction Works Step-by-Step

1. Preparing the Transaction

Alice wants to send 1 BTC to Bob. She enters Bob’s account address, specifies the amount, and signs it using her private key. This generates a digital signature that authorizes the transaction.

2. Broadcasting the Transaction

Once signed, Alice’s transaction is broadcast to the Bitcoin network.

3. The Role of Miners & Proof-of-Work

Miners pick up the transaction and attempt to add it to the blockchain. To do this, they must solve a complex mathematical puzzle known as proof-of-work. The first miner to solve it earns the right to add Alice’s transaction to a new block and receives a reward.

4. Recording the Transaction

The transaction becomes part of a block. This block is linked chronologically to previous blocks, forming the blockchain.

5. Consensus

All nodes verify that their copies of the blockchain match and that Alice’s transaction is valid. This ensures agreement across the entire network.

6. Completion

Once consensus is reached, the 1 BTC is officially transferred from Alice to Bob. When Bob checks his Bitcoin wallet, he sees his new balance.

Why Use Blockchain?

- Faster Transactions: Cross-border payments can complete in minutes instead of days.

- Lower Costs: Instead of paying high fees (e.g., 2% on a $10,000 credit card payment), only a small network fee is charged.

- No Intermediaries: Alice and Bob transact directly without banks or paperwork.

- Transparent Records: All data is stored on a distributed ledger, visible anytime.

- Enhanced Security: Cryptography and decentralization make tampering nearly impossible.

- Fraud Prevention: Since anyone can independently verify transactions, it’s very hard to forge payments or misappropriate funds.

Prerequisites

- Basic JavaScript knowledge

- Understanding of web development concepts

- Familiarity with command line interface

- Basic cryptography concepts

What You Will Learn

- Blockchain fundamentals and architecture

- Smart contract development with Solidity

- Building decentralized applications (DApps)

- Working with Web3.js and Ethereum

- Deploying contracts on testnets and mainnet

- Security best practices for blockchain development

- Testing and debugging smart contracts

- Integrating blockchain with frontend applications

Ready to Start Learning?

Begin your journey with the first topic and work your way through the complete tutorial.